A Comprehensive Guide to Fintech Software Development in 2026

Shailesh Gujjar

Published: Apr 10, 2026

Key Takeaways:

Fintech software development in 2026 is driven by innovation, but success depends on balancing technology with compliance, security, and user trust.

Building a fintech product is not just about features; it’s about creating seamless, secure, and scalable financial experiences.

From AI to open banking, emerging technologies are reshaping how financial services are built, delivered, and consumed.

The development approach you choose, MVP vs full-scale platform, directly impacts cost, time-to-market, and long-term growth.

Partnering with an experienced fintech development company can make the difference between a product that launches and one that actually succeeds.

Think about the last time you walked into a bank branch to do something important. For most people under 40, that memory is becoming increasingly difficult to recall.

Today, you transfer money while commuting, get a loan approved in minutes without paperwork, and invest in fractional shares before your morning coffee.

None of that happens without powerful fintech software development running silently in the background.

As per the report published by Fortune Business Insights, the global fintech market was valued at $394.88 billion in 2025 and is projected to reach $460.76 billion in 2026, growing at an 18.2% CAGR toward $1.76 trillion by 2034.

Generally, people define fintech software as just software for finances, but there’s more to this story. It is a very different process from the other software, as it requires expertise in financial regulations, real-time data processing, fraud prevention, multi-party integration, and tight security; everything at once. It takes everything to be done very precisely and securely.

This guide is made specifically for 2026, a year where AI in fintech is exploding, embedded finance is reshaping entire industries, and digital banking software development is moving faster than ever.

Whether you’re a startup founder evaluating your first fintech platform development project, a product leader at an established bank exploring custom fintech software development, or a CTO assessing vendors for financial app development, this guide is your complete reference.

We’ll cover what fintech software development actually involves, break down every type of app, walk through the development lifecycle step by step, give you a frank look at real fintech app development costs, and show you exactly what separates a fintech development partner worth hiring from one that will slow you down.

Fintech Market Growth & Opportunities in 2026

The numbers don’t lie, and in 2026, they’re telling a story of extraordinary expansion. Fintech is no longer a challenger to traditional banking. In many segments, it has become the mainstream choice for consumers and businesses alike.

The year 2026 will experience growth due to multiple forces that are currently converging.

Consumer expectations have permanently shifted. People now expect instant digital-first financial services, which require digital access. The app experience now serves as the basic requirement for users.

The regulatory environment has reached its advanced stage. The EU, US, UK, India, and Southeast Asian countries have established their regulatory sandboxes, which provide new businesses with safer operational frameworks.

AI technology enables fintech companies to develop innovative business models through its application to their operations. Artificial intelligence now powers the financial technology sector to provide immediate fraud detection services while developing customized lending products that were impossible to create two years ago.

B2B fintech companies represent the industry’s most recent development. The $5 trillion SME credit gap and embedded finance growth require B2B and B2B2X fintech models, which now receive disproportionate amounts of funding and industry focus.

The Asia-Pacific region serves as the main driver of growth for the world economy. The Asia-Pacific region will become the biggest fintech market worldwide by 2030 as it grows at a 27% annual growth rate, with China, India, and Indonesia.

For any business considering fintech software development today, the market timing couldn’t be more compelling. The infrastructure is mature, the user base is ready, and the technology has never been more capable.

What is Fintech Software Development?

The process of developing Fintech software involves designing and building digital products that provide automated financial services. The product development process integrates financial domain expertise, which includes transaction logic, regulatory requirements, and risk modeling, with engineering capabilities, which cover scalable architecture, security, and system integrations to create products that allow secure and efficient money management.

The term encompasses a wide range of results, which include a basic payment application that enables freelancers to receive payments through their mobile phones, a banking software development project that modernizes an outdated core banking system, and a digital banking software development project that enables a neobank to provide services to millions of customers without needing physical branches and all other developed elements.

What makes financial software development different from general software development? Three things primarily:

1. Regulatory complexity: The financial applications need to follow different regulatory requirements, which depend on the specific market, because they must comply with PCI-DSS for card payments and GDPR for EU user data and KYC/AML laws, which apply worldwide, and the unique regulations that govern banking, lending, and insurance sectors.

2. Security requirements: Cybercriminals view financial data and real money as their most valuable targets. The attack methods used against fintech applications reach a level of complexity that other software types do not experience.

3. Integration depth: Fintech applications need to connect with multiple systems, which include core banking networks, payment systems, KYC providers, credit bureaus, and other fintech services through open banking APIs. The process of adding new integrations creates additional difficulties because it introduces possible delays and creates new requirements for compliance.

Software development for fintech also demands a different team profile. You need developers who understand financial concepts like double-entry bookkeeping, reconciliation, and settlement cycles, not just engineers who can build a CRUD application quickly.

The stakes are also uniquely high. A bug in a social media app causes user frustration. A bug in a payment app can cause real financial harm to real people. That responsibility shapes every design decision in legitimate fintech development.

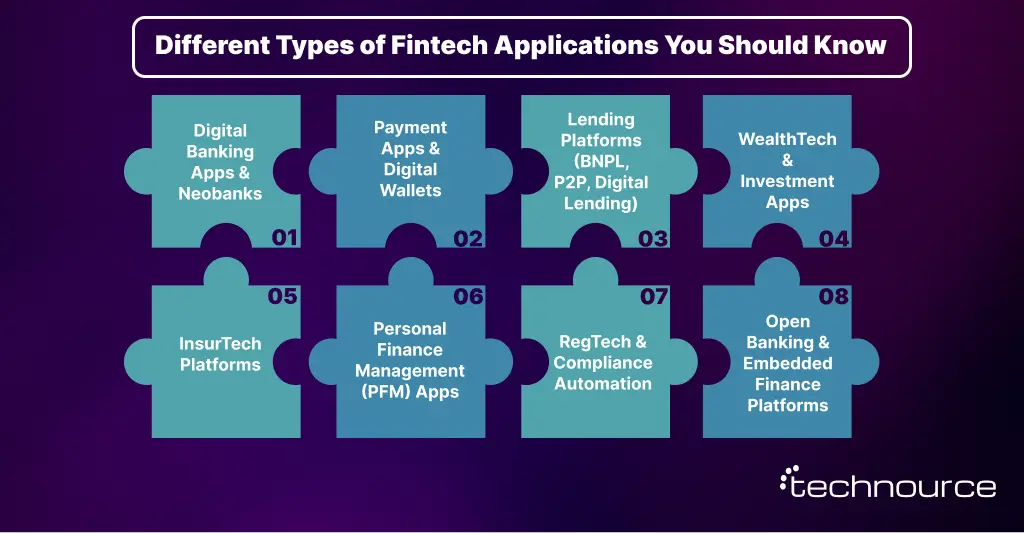

Types of Fintech Applications with Real-World Examples

Not all fintech apps are built the same. A neobank and a BNPL platform are both “fintech” on paper, but they share almost nothing in terms of architecture, compliance requirements, or what it costs to build them. Knowing your category upfront changes every decision that follows, especially when building top finance applications that need to scale and comply from day one.

1. Digital Banking Apps & Neobanks

Revolut hit 50 million users. Chime became one of America’s most valuable private companies without owning a single branch. The neobank model works, and the software behind it is anything but simple.

Managing a real-time ledger at scale, building KYC flows that regulators accept and users don’t abandon halfway through, integrating card issuance with Visa or Mastercard’s own compliance requirements on top of yours, banking software development is a different discipline from regular app development.

Examples: Revolut, Chime, Monzo, Jupiter, NuBank

Hard Parts: Core banking integrations, real-time reconciliation, regulatory capital requirements

2026 Shift: AI spending insights are now table stakes. Cross-border instant transfers are an expectation, not a premium.

2. Payment Apps & Digital Wallets

Payments is the largest fintech category by revenue, roughly 55% of all scaled fintech income globally. Every business needs to collect money. Every consumer needs to move it.

The payment app development process establishes rewards for teams that have completed the task before and creates disadvantages for teams that fail to recognize its complexity.

Examples: PhonePe, Google Pay, PayPal, Stripe, Razorpay

Hard Parts: Multi-rail integration, chargeback handling, real-time fraud ML

2026 Shift: Stablecoin payments entering B2B cross-border. Embedded payments growing fastest money movement built invisibly into non-finance products.

3. Lending Platforms (BNPL, P2P, Digital Lending)

The digital lending system has shortened the loan approval process, which used to take weeks, until it now requires only a few minutes.

The credit decisioning engines and KYC/bureau integrations, repayment management, and collections workflows that power this system represent the most advanced technology in the fintech industry.

Hard parts: Alternative credit scoring, ML underwriting that needs continuous retraining, BNPL regulation now active in EU/UK/Australia

2026 shift: Open banking transaction data replacing bureau scores for the unbanked.

4. WealthTech & Investment Apps

Robinhood created a mobile-first investing platform that required no commission fees. The same service was introduced to India by Groww and Zerodha. The market experienced an influx of millions of first-time retail investors who started participating in trading activities. The system contains multiple components that deliver real-time market data, manage order routing, create tax reporting systems, and ensure compliance with SEBI and SEC regulations.

Hard Parts: Low-latency data feeds, compliant order execution, per-jurisdiction tax reporting

2026 Shift: Tokenized real-world assets appearing on retail platforms. AI portfolio managers are replacing basic robo-advisors.

5. InsurTech Platforms

Insurance is one of the last financial categories still drowning in paper. Lemonade handles some claims in under three seconds using AI.

That’s not marketing it’s what happens when you rebuild the claims process in software from scratch instead of digitizing old paper workflows.

Examples: Policybazaar, Digit Insurance, Acko

Hard Parts: Policy admin systems, actuarial logic in code, IoT/telematics data pipelines, highly variable regulation by jurisdiction

2026 Shift: Embedded insurance at checkout (travel, device, delivery) is growing fast and demanding API-first architecture.

6. Personal Finance Management (PFM) Apps

PFM apps don’t hold money or process payments; they just help people understand all of it in one place. That sounds simple. Connecting reliably to dozens of banks, normalizing inconsistent transaction data, and categorizing spending accurately enough to be useful is a real data engineering problem.

Examples: Mint, YNAB, Walnut, Fi Money

Hard Parts: Open banking aggregation coverage and reliability, ML-based transaction categorization

2026 Shift: Moving from passive dashboards to active AI financial coaches that prompt action, not just display numbers.

7. RegTech & Compliance Automation

Compliance costs at major banks can exceed $1 billion a year. Software that automates even a portion of that is an easy sell. RegTech is quietly one of the fastest-growing fintech investment areas.

Examples: ComplyAdvantage, Onfido, Signzy, Napier AI

Hard Parts: Real-time sanctions list updates, transaction monitoring tuned to minimize false positives without missing real threats, tamper-evident audit trails

2026 Shift: DORA compliance tooling in demand across the EU. Crypto AML monitoring is now mandatory in most major markets.

8. Open Banking & Embedded Finance Platforms

Embedded finance is the bet that financial services’ future isn’t in dedicated apps, it’s woven into the software people already use. Shopify lending to its merchants. Uber is advancing earnings to drivers.

The BaaS infrastructure powering all of that is the most architecturally complex category in fintech; you’re not building one product, you’re building a platform that other products run on.

Hard Parts: Multi-tenant architecture, compliance pass-through, partner bank integrations that each behave differently

2026 Shift: B2B embedded finance, working capital in procurement software, and FX in ERP systems is where the next wave of growth is coming from.

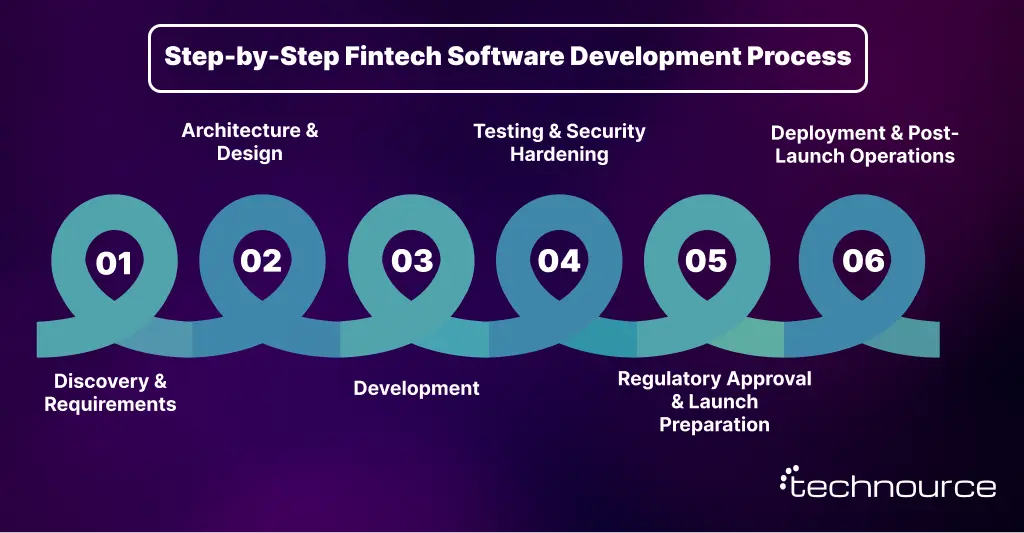

Fintech Software Development Lifecycle: Step-by-Step Process

The teams that run into the most trouble in fintech aren’t usually the ones with bad engineers. They’re the ones that treated financial software development like normal app development and got blindsided by what’s different about it: compliance surprises in month five, security architecture that wasn’t designed for the actual threat model, and integrations that took three times longer than estimated.

Every phase below matters. Shortcuts in Phase 1 create expensive problems in Phase 3. Gaps in Phase 4 create production incidents after launch.

Phase 1: Discovery & Requirements (Weeks 1–4)

The most important phase. Also, the most frequently rushed because it doesn’t produce visible code, which is exactly the wrong way to think about it.

In fintech, discovery isn’t just writing user stories. It’s determining your regulatory environment before architecture decisions get made, identifying integration dependencies before timelines get set, and doing threat modeling before security architecture gets designed. Skipping this work doesn’t make it disappear. It just moves it to a more expensive moment.

Business requirements: User journeys, revenue model, target segments, success metrics; defined clearly enough that there’s no ambiguity when development starts.

Regulatory scoping: Which frameworks apply, PCI-DSS, GDPR, KYC/AML, RBI, DORA? This determines architecture choices that you cannot easily change later.

Build vs. buy decisions: Do you build KYC in-house or use Onfido? Process payments directly or through Razorpay? These should be deliberate choices, not defaults.

Threat modeling: What data are you protecting? What are the realistic attack vectors? What’s the blast radius of different failure scenarios?

Phase 2: Architecture & Design (Weeks 3–6)

Architecture is where fintech products get their structural DNA. The decisions made here, microservices vs. monolith, database choices, security model, API development and design, will define the product’s scalability and compliance posture for years. This is not a phase to staff with junior engineers or rush through.

System architecture: Microservices make sense at scale. A 3-person team building an MVP doesn’t need 15 independent services. Make the choice deliberately based on your actual requirements, not what sounds most sophisticated.

Data architecture: Where does data live? Who can access it? Data residency rules in the EU, India, and China mean your cloud and database choices are compliance decisions, not just technical ones, making data engineering solutions essential for designing compliant, secure, and scalable data architectures.

Security architecture: Zero trust networking, WAF, secrets management, DDoS protection, designed in from the start, not retrofitted after the first incident

UI/UX design: Fintech UX has to feel effortless while simultaneously signaling trustworthiness. Those goals are in tension, and resolving that tension is what separates good fintech design from generic app design.

Phase 3: Development (Weeks 6–24+)

Agile sprints are typically two weeks. The one hard rule that distinguishes fintech development from general software: security review is part of every sprint, not a gate at the end. Financial logic is reviewed only at launch, ships with exploitable vulnerabilities.

Backend: The financial logic layer, transaction processing, reconciliation, interest calculations; needs engineers who understand distributed systems and financial concepts. Getting lending interest calculations wrong isn’t just a bug; it’s a regulatory violation.

Mobile (fintech mobile app development): For high-security apps, crypto wallets, trading platforms, anything biometric, native development (Swift/Kotlin) is the right call. The iOS Secure Enclave and Android Keystore don’t have reliable cross-platform equivalents. For MVP-stage, lower-security products, React Native or Flutter is a legitimate cost optimization.

Integration work: Consistently underestimated. Partner API documentation is usually incomplete. Sandbox environments don’t behave like production. Budget 2–3x your initial estimate for any integration that involves a bank or payment network

Infrastructure: CI/CD with security scanning gates, monitoring, and alerting configured before go-live; not after your first production incident

A bug in an e-commerce app means the wrong item ships. A bug in a payment app means someone’s money goes somewhere it shouldn’t. The stakes are different, and the testing discipline has to match.

Penetration testing: Third-party pen tests are required by most card network agreements, many banking partner contracts, and several regulatory frameworks directly. Budget $15,000–$50,000 and book 3–4 months in advance; reputable firms fill up.

Load & stress testing: Payment systems need to handle volume spikes without degrading. Test for 3–5x your expected peak, not your expected average.

Compliance testing: KYC flows, audit trail completeness, data handling, verified against your specific regulatory requirements, not generic checklists.

Security code review: SAST/DAST tools plus manual review for any code path that touches financial transactions or sensitive data.

Phase 5: Regulatory Approval & Launch Preparation

For licensed products neobanks, lending platforms, payment institutions regulatory approval is a standalone phase. Depending on jurisdiction and product type, this adds 3–12 months. Teams that don’t plan for this timeline end up with finished software sitting idle while waiting for approvals. Build it into the project plan from day one.

Phase 6: Deployment & Post-Launch Operations

Staged rollout: Blue-green deployments and feature flags go-live risk is real in fintech, and canary releases catch problems before they affect all users

Monitoring: Real-time transaction monitoring, anomaly detection, 24/7 alerting. In financial software, you want to know about a problem before your users do

Ongoing compliance: Regulations evolve. DORA, RBI updates, new AML guidelines, your compliance posture needs active maintenance, not a set-and-forget approach

Iteration: Analytics-driven feature improvement, A/B testing, and regular security patching. The product doesn’t stop needing investment after launch.

Essential Features of Modern Fintech Software (Checklist)

Building a fintech application without the right features is like opening a bank with no vault. Below is a comprehensive checklist covering core functionality, security, compliance, and user experience, applicable to financial app development across all major categories.

Core Functionality

User registration and digital onboarding

KYC (Know Your Customer) verification with document scanning and liveness detection

API management and developer portal (for B2B/embedded products)

Fintech Tech Stack: Technologies Behind Modern Financial Apps

The technology choices in fintech software development directly impact security, scalability, regulatory compliance, and long-term maintenance costs. Here’s what mature fintech teams are building in 2026.

Backend Technologies

Technology Area

Tools & Languages

Purpose in Fintech Apps

Primary Language

Java, Go, Python, Node.js (TypeScript)

Java & Go favored for high-throughput transaction processing; strong type systems reduce financial logic bugs

API Framework

Spring Boot, Gin, FastAPI, NestJS

REST + GraphQL; gRPC for internal microservices where latency matters

Primary Database

PostgreSQL, CockroachDB, MySQL

ACID compliance is non-negotiable for financial transactions

Time-series / Analytics

ClickHouse, TimescaleDB, Redshift

Transaction history analytics, fraud pattern analysis, and regulatory reporting

Caching

Redis, Memcached

Session management, rate limiting, OTP storage with TTL

Message Queue

Apache Kafka, RabbitMQ, AWS SQS

Async transaction processing, event sourcing, and audit log streaming

Search

Elasticsearch, OpenSearch

Transaction search, fraud case management, compliance queries

Mobile Technologies (Fintech Mobile App Development)

Fintech Software Architecture: How Scalable Systems Are Built

Architecture is where fintech products succeed or fail at scale. A payment app processing 100 transactions per day has fundamentally different architecture needs than one processing 100 transactions per second. Poor architecture choices compound over time, leading to outages, security vulnerabilities, and expensive re-platforms.

1. Microservices Architecture

The dominant architectural pattern for modern fintech software development. Instead of one monolithic application, the system is split into independently deployable services, each owning a specific business domain (accounts, payments, KYC, notifications).

Why fintech loves microservices: Independent scaling (scale only the payment service during high demand), independent deployment (update fraud rules without touching the payments engine), better fault isolation (a KYC service failure doesn’t take down the whole app).

The challenge: Distributed systems are harder to debug, and transaction consistency across services requires careful design using patterns like Sagas and event sourcing.

2. Event-Driven Architecture (EDA)

Financial events (payment initiated, KYC completed, fraud flagged) trigger downstream processes asynchronously. Apache Kafka is the industry standard here. EDA enables real-time analytics, immutable audit trails, and decoupled integrations.

3. CQRS + Event Sourcing

Command Query Responsibility Segregation (CQRS) separates write operations from read operations. Combined with event sourcing (storing every state change as an immutable event), this pattern is particularly valuable in financial software development — it provides a complete, tamper-evident audit trail that regulators love.

4. API Gateway & BFF Pattern

A central API gateway manages authentication, rate limiting, and routing. The Backend-for-Frontend (BFF) pattern creates tailored APIs for mobile and web clients — critical in fintech mobile app development, where mobile experiences differ significantly from web.

5. Zero Trust Security Model

Traditional security assumed internal network traffic was safe. Zero trust assumes the opposite: verify every request, regardless of whether it comes from inside or outside the network perimeter. In 2026, zero trust is the expected baseline for any serious fintech platform.

6. Multi-Region & Disaster Recovery

Production fintech systems must be designed for resilience from day one. This means active-active or active-passive multi-region setups, RPO (Recovery Point Objective) and RTO (Recovery Time Objective) defined at the architecture stage, and regular DR drills. Regulators increasingly require documented disaster recovery capability.

Security & Compliance in Fintech Software Development

Security in fintech isn’t a feature — it’s the foundation. A single serious breach can end a fintech company. Getting compliance right from the start is also dramatically cheaper than retrofitting it after the fact.

Security in 2026 is a core product requirement, not just compliance. Fintech apps must adopt proactive, multi-layered security to handle evolving threats like deepfakes and complex integrations.

1. Biometric Liveness 3.0: In 2026, deepfake fraud grew over 1,000% in some markets. Standard selfie liveness checks are no longer sufficient. Advanced liveness detection, analyzing micro-expressions and skin light reflection, is now the expected standard for KYC in high-value financial apps.

2. Encryption everywhere: AES-256 at rest, TLS 1.3 in transit, field-level encryption for particularly sensitive data (SSN, bank account numbers). Certificate pinning in mobile apps to prevent MITM attacks.

3. Threat modeling from day one: STRIDE methodology applied during the architecture phase. Every new feature is evaluated for security implications before development begins.

4. Shift-left security: SAST (static analysis) and DAST (dynamic analysis) tools integrated into the CI/CD pipeline. Security issues caught in development cost 10x less to fix than post-launch.

5. Third-party vendor security: Fintech apps integrate many third-party services. Each integration is an attack surface. Vendor security assessments, contractual security requirements, and regular re-assessments are essential.

Fintech Business & Monetization Models

A common mistake in fintech platform development is treating the monetization model as an afterthought. In reality, how your fintech makes money shapes architectural decisions (billing systems, usage metering), compliance requirements (licensing for certain revenue models), and product design.

Monetization Model

How It Works

Common Use Cases

Examples

Transaction fees

Percentage or flat fee per transaction

Payment apps, neobanks, lending platforms

Stripe (2.9% + 30¢), Razorpay

Subscription/SaaS

Monthly/annual fee for access

PFM apps, RegTech, B2B fintech tools

YNAB ($14.99/mo), Plaid

Interchange revenue

Share of interchange from card transactions

Neobanks with card products

Chime, Revolut

Interest income / NIM

Interest spread between lending and deposit rates

Neobanks, BNPL, lending platforms

Affirm, LendingClub

Freemium to premium

Free tier + paid advanced features

Investment apps, PFM, crypto wallets

Groww, Robinhood Gold

Data monetization (B2B)

Aggregated/anonymized insights to FIs

PFM apps, open banking platforms

Plaid, Finbox

White-label/BaaS licensing

License the platform to other businesses

Core banking SaaS, payment infrastructure

Mambu, Marqeta

Key insight: McKinsey projects fintech revenues will grow almost 3x faster than traditional banks from 2022 to 2028. The businesses building fintech infrastructure today are positioned to capture this growth — but only if their software is built for scale from day one.

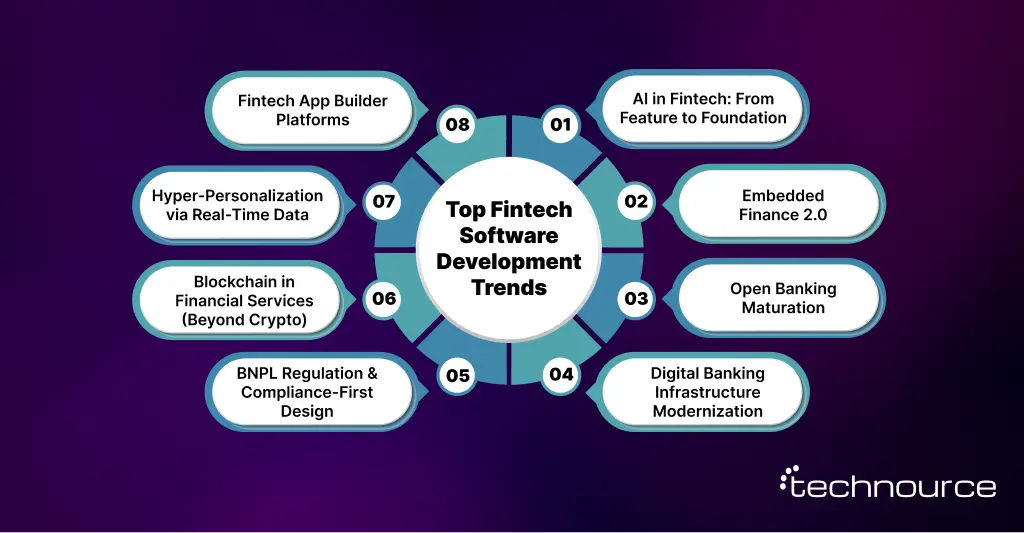

Top Fintech Software Development Trends in 2026

The fintech landscape in 2026 looks materially different from just two years ago. Here are the trends that are reshaping how financial app development teams think, build, and compete.

1. AI in Fintech: From Feature to Foundation

AI in fintech has moved well past the proof-of-concept stage. In 2026, AI isn’t a premium add-on; it’s embedded in core workflows across fraud detection, credit decisioning, customer service, and investment management.

Generative AI for financial advice: LLM-powered chatbots that can explain complex financial products in plain language, generate personalized savings plans, and answer tax-related questions.

ML-based fraud detection: Real-time models that analyze hundreds of signals per transaction to flag anomalies, far outperforming rule-based systems.

Alternative credit scoring: AI models using non-traditional data (utility payments, rental history, device usage patterns) to extend credit to the 1.4 billion unbanked adults worldwide.

AI-powered KYC: Document verification and liveness detection that processes in seconds with accuracy exceeding human review.

2. Embedded Finance 2.0

Embedded finance, the integration of financial services into non-financial products, is in its second, more sophisticated wave. Where the first wave was mostly about “pay here” buttons, Embedded Finance 2.0 involves deeply integrated, personalized financial products within the user flows of SaaS platforms, e-commerce sites, and enterprise software.

The global embedded finance market is projected to reach $197 billion in 2026, growing toward $646 billion by the end of the decade. Software development fintech teams focused on BaaS platforms and API-first infrastructure are at the center of this growth.

3. Open Banking Maturation

PSD2 in Europe opened the door; now markets from India (AA framework) to Australia (CDR) to Brazil (Open Finance) are implementing open banking mandates. This creates both compliance obligations and opportunities for fintech API integration across the ecosystem.

4. Digital Banking Infrastructure Modernization

Major banks are finally replacing their 1970s-era core banking systems with modern, cloud-native alternatives. Digital banking software development opportunities in core modernization, API-first banking, and cloud migration are among the largest enterprise tech deals being signed in 2026.

5. BNPL Regulation & Compliance-First Design

Buy Now Pay Later exploded during 2020–2023, and regulators worldwide are now catching up. In 2026, BNPL providers face formal regulation in the EU, UK, India, Australia, and several US states. Financial app development in the lending space now requires compliance-first architecture from the ground up.

6. Blockchain in Financial Services (Beyond Crypto)

The blockchain conversation in fintech has matured considerably. In 2026, the most impactful blockchain use cases, often delivered by a trusted blockchain development company, aren’t about cryptocurrency speculation — they’re about settlement efficiency, cross-border payment infrastructure, tokenized real-world assets (RWAs), and programmable compliance via smart contracts.

7. Hyper-Personalization via Real-Time Data

The combination of open banking data, AI models, and real-time processing enables financial products that adapt to individual behavior, personalized interest rates, dynamic spending limits, and proactive savings recommendations.

Custom fintech software development gives companies the ability to leverage proprietary data in ways that off-the-shelf solutions never can.

8. Fintech App Builder Platforms

For lower-complexity use cases, no-code and low-code fintech app builder platforms are gaining traction particularly for internal financial tools, simple payment collection, and B2B invoicing.

However, these platforms have hard ceilings on customization, security controls, and regulatory compliance that make them unsuitable for regulated fintech products at scale.

Fintech Software Development Cost in 2026: Complete Breakdown

This is one of the most searched and most poorly answered questions in fintech. Vague ranges like “$50K to $500K” are useless without context. Let’s break it down properly.

Quick benchmark: Fintech app development cost in 2026 ranges from approximately $20,000 for a narrow MVP to $300,000+ for a full-featured platform, and enterprise-grade products can exceed $1 million when compliance, security hardening, and operational tooling are fully scoped.

Security patches, compliance updates, feature iteration, and infrastructure costs

Factors That Drive Fintech Development Costs Up

1. Regulatory complexity: Building for multiple jurisdictions simultaneously multiplies compliance costs. Every new market adds localization, additional licensing, and regulatory reporting requirements.

2. Security requirements: Advanced biometric authentication, third-party pen testing, security audits, and ongoing vulnerability management add $30K–$100K+ to a typical project.

3. Third-party integration depth: Integration with payment rails, credit bureaus, and banking cores takes roughly 15–20% of a typical fintech app budget — and more if the partners have poor API documentation.

4. Team location: US/UK senior fintech engineers cost $150,000–$200,000+ per year in salary alone. Indian development teams typically run $25–$50/hour, making offshore partners a compelling option for cost management.

5. Architecture choices: Microservices done right cost more upfront than a monolith, but typically save significant money over the 3–5 year horizon through easier scaling and maintenance.

How to Reduce Fintech App Development Costs Without Sacrificing Quality

Step 1: Start with a focused MVP to resist the temptation to build every feature immediately

Step 2: Use pre-built, regulated infrastructure (Stripe for payments, Onfido for KYC) instead of building from scratch

Step 3: Work with an experienced fintech development partner who won’t learn compliance on your budget

Step 4: Choose cross-platform mobile for MVPs in lower-security categories — native for security-critical products

Step 5: Plan your regulatory roadmap early to avoid expensive late-stage compliance retrofits

Step 6: Use managed cloud services to reduce DevOps overhead in early stages

Key Challenges in Fintech Software Development

Fintech development is rewarding precisely because it’s hard. Here are the challenges that trip up even experienced teams — and how to approach them.

1. Regulatory Uncertainty and Change: Regulations governing fintech are actively evolving in most major markets. The EU’s DORA regulation (operational resilience) took effect in early 2025 with significant implications for all financial technology providers.

India’s RBI regularly updates its payment and lending regulations. Building systems that can adapt to regulatory change without full re-platforms requires a modular compliance architecture.

2. Security at Scale: The threat landscape for financial software escalates continuously. Deepfake-assisted identity fraud, API attacks, and supply chain compromises are all growing threats in 2026. Security can’t be a one-time project — it requires ongoing investment, monitoring, and response capability.

3. Legacy Integration Complexity: Most banks and financial institutions still run core systems built decades ago. Building modern fintech apps that integrate with these systems requires understanding legacy API formats (ISO 8583, SWIFT MT messages), building robust error handling for unreliable legacy endpoints, and managing data format transformation.

4. Talent Scarcity: Finding engineers who combine software development expertise with deep financial domain knowledge is genuinely difficult. This is one of the strongest arguments for partnering with a specialized fintech software development company rather than building an in-house team for a first product.

5. Scaling Financial Systems: Scaling a fintech app isn’t just about adding servers. Financial transactions require strong consistency guarantees that general-purpose horizontal scaling approaches don’t provide. Designing for scale in fintech requires careful distributed systems architecture from the beginning.

6. Third-Party Dependency Risk:Fintech products depend on external providers (payment rails, KYC vendors, banking cores) whose outages become your outages. Designing for provider redundancy, graceful degradation, and monitoring third-party SLAs is an essential operational practice.

7. Building and Maintaining User Trust: Trust is the ultimate currency in fintech. One security incident, one prolonged outage, or one compliance failure can permanently damage user trust in ways that are very hard to recover from. This means that quality assurance and security aren’t just technical concerns — they’re business-critical priorities.

How to Choose the Right Fintech Software Development Company

Choosing the right fintech partner can define your product’s success. Focus on what truly matters in real-world delivery, not just polished sales pitches.

What to Look for:

Fintech expertise with real, relevant case studies

Compliance experience with regulations like PCI-DSS, RBI, and GDPR

Scalable architecture thinking, not one-size-fits-all solutions

Proven integrations with payment gateways, KYC, and banking systems

Clear pricing and long-term support, not just project delivery

Quick Questions to Ask:

Can you share real fintech projects with regulatory challenges?

How do you handle security testing throughout development?

What integrations have you worked on in production?

How do you manage scope or compliance changes mid-project?

What does your post-launch support look like?

Real-World Implementation Insights from Fintech Projects

At Technource, fintech projects are rarely just about building features. The real challenge is simplifying complex financial workflows while keeping systems secure and scalable.

For instance, while developing a digital loan platform like Cashguru the goal was to make borrowing simple for users. Instead of dealing with multiple lenders separately, users could compare loan options, check eligibility, and apply in one place.

The complexity came from handling loan logic approvals, tenure, and eligibility checks. To manage this, the platform was built with a modular backend and real-time data handling to ensure accurate results and faster processing.

In another project, like Suitme, a crypto trading and staking platform, the focus was completely different. Here, real-time transactions, asset management, and security were critical.

The system needed to handle live price updates, seamless trading experiences, and secure user transactions without delays or risks.

Across both projects, a few things remained constant:

Real-time data processing is essential

Security cannot be compromised

Systems must scale with users and transactions

These experiences show that fintech software development isn’t just about building apps; it’s about creating reliable systems that can handle financial complexity in the real world.

Why Choose Technource for Fintech Software Development

Technource combines deep fintech expertise with a practical, security-first approach to building real-world financial products. With experience across payments, banking, lending, and InsurTech, we focus on delivering solutions that are not just functional but scalable, compliant, and built to last.

What sets us apart:

1. Domain expertise that matters: We’ve built and scaled real fintech products, not just generic applications.

2. Security-first mindset: From architecture to deployment, compliance and data protection are embedded at every stage.

3. End-to-end capabilities: Whether it’s an MVP or an enterprise platform, we handle everything from backend systems to user-facing apps.

4. Transparent, Agile delivery: Clear timelines, regular demos, and no hidden surprises.

5. Proven integrations: Experience with payment gateways, KYC providers, and banking systems ensures faster execution.

How to Get Started with Fintech Software Development

Starting a fintech product requires more than just a good idea—it demands clarity, planning, and the right execution strategy. Begin by clearly defining the financial problem you’re solving, your target users, and what makes your solution different.

At the same time, identify the regulatory requirements relevant to your market early on to avoid costly surprises later.

Instead of building everything at once, focus on developing MVP that delivers real value and can be tested quickly in the market. Choose a development partner who not only understands technology but also fintech-specific challenges, as this will impact your product’s scalability and compliance.

Finally, plan beyond the launch—fintech products require ongoing security updates, compliance checks, and feature improvements to stay competitive and reliable. If you’re looking to build a secure and scalable fintech solution, contact us to get expert guidance and turn your idea into a successful product.

Conclusion:

Fintech in 2026 offers massive opportunities, but opportunities don’t capture themselves. Building a successful fintech product requires getting the foundations right: understanding your regulatory environment before writing a single line of code, architecting for security and scale from day one, choosing integrations that give you speed-to-market without technical debt, and working with development partners who bring genuine financial domain expertise, not just general engineering ability.

From regulatory readiness and secure architecture to the right integrations and expert partners, every decision shapes your product’s future. The winners in fintech aren’t just those who build fast, but those who build smart, stay compliant, and continuously evolve with the right team by their side.

FAQs

Fintech software development is the process of building digital products and platforms that deliver, automate, or enhance financial services, including payments, banking, lending, investment, insurance, and compliance tools. It combines software engineering with financial domain expertise, regulatory knowledge, and cybersecurity.

Timeline depends heavily on app type and complexity. A focused MVP typically takes 3–6 months. A full-featured payment app or digital banking product takes 8–18 months. Regulated products that require licensing approval can add 3–12 months to these timelines.

Fintech app development costs range from approximately $20,000 for a narrow MVP to $300,000+ for a full-featured platform. Enterprise-grade products with full compliance, security hardening, and operational infrastructure can exceed $1 million. Key cost drivers include regulatory complexity, security requirements, third-party integrations, and team location.

Evaluate potential partners on fintech-specific domain expertise, security practices (not just general statements but specifics like their secure SDLC approach and pen testing experience), compliance knowledge relevant to your market, their integration track record with payment gateways and banking systems, post-launch support model, and their willingness to give you direct access to engineers and real client references.

Custom fintech software development means building financial software tailored specifically to your business requirements, rather than implementing an off-the-shelf or white-label solution. It offers competitive advantages through proprietary workflows, unique data utilization, specific compliance configurations, and deep integration with your existing systems at the cost of higher initial investment and longer timelines.

Shailesh Gujjar is a Team Leader at Technource with over 10 years of experience as a web and mobile development expert. He specializes in JavaScript technologies like Node.js, React, and Angular, as well as mobile platforms including native Android, Flutter, and React Native. Shailesh leads end-to-end development projects, ensuring secure, high-performance solutions through strong technical and leadership capabilities.

Request Free Consultation

Amplify your business and take advantage of our expertise & experience to shape the future of your business.